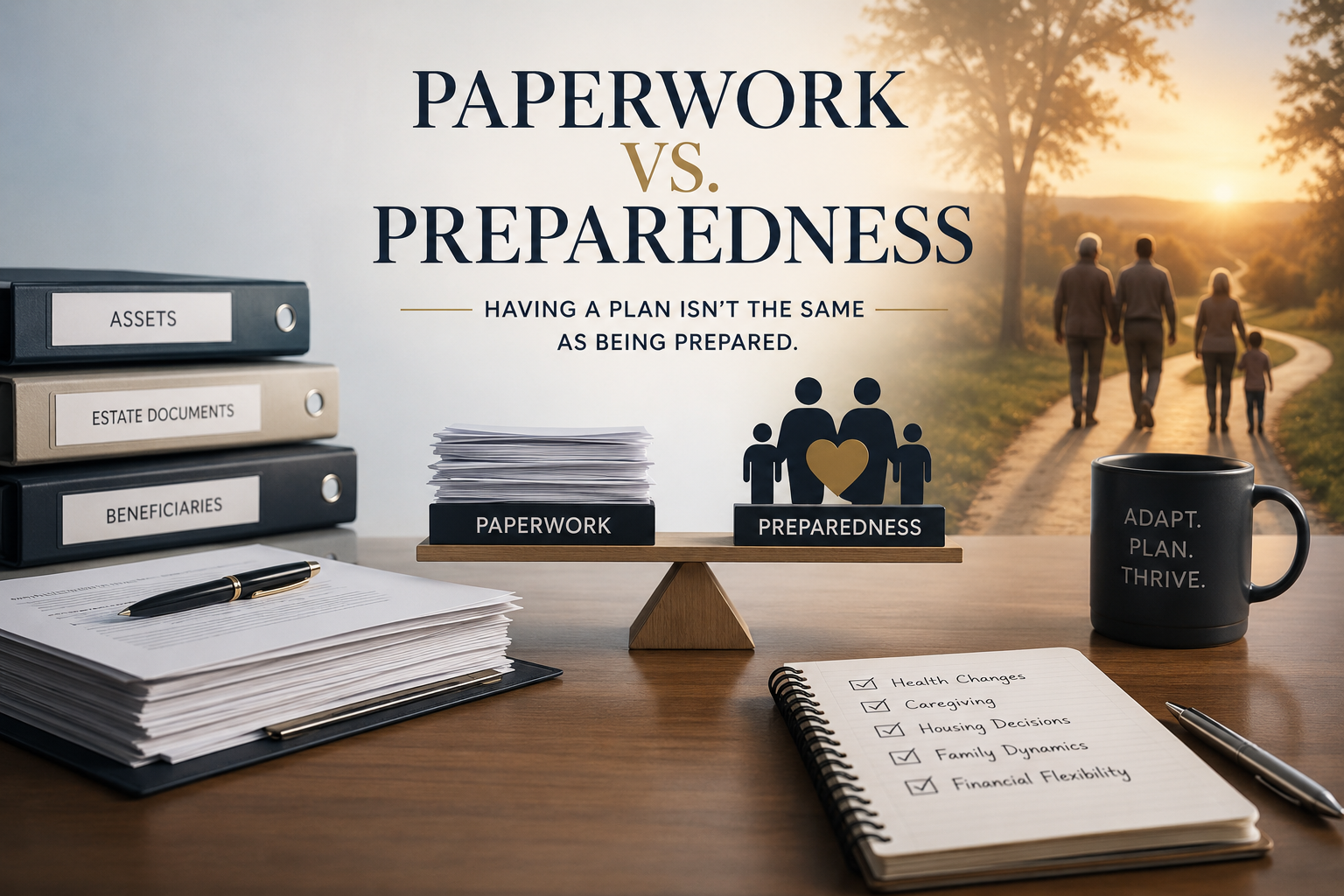

Paperwork vs. Preparedness: Why Estate Plans Alone Aren’t Enough

Retirement Strategist Carroll Golden

Everything Looks Fine on Paper

Many clients appear fully prepared.

They have assets.

They have estate documents.

They have beneficiaries designated.

Their financial lives are organized, documented, and seemingly under control.

From a planning perspective, all the boxes have been checked.

But preparedness and organization are not the same thing.

One of the most common misconceptions in retirement planning is believing that once the paperwork is complete, the work is done.

In reality, that's often when the real questions begin.

The Illusion of Being Ready

The families who appear most prepared on paper can still find themselves struggling when life takes an unexpected turn.

Not because they forgot a document.

Not because they failed to create an estate plan.

But because the challenges that disrupt retirement rarely originate from paperwork.

They come from life itself.

A spouse's health begins to decline.

A parent suddenly needs ongoing care.

An adult child moves back home after a major life transition.

A housing decision becomes urgent after an illness, injury, or loss.

These situations don't ask whether your documents are organized.

They ask whether your plan can adapt.

When Retirement Meets Reality

Retirement planning is often built around assumptions.

We assume health will remain stable.

We assume family circumstances will stay relatively consistent.

We assume decisions can be made thoughtfully and without urgency.

Yet longevity has changed the equation.

People are living longer than ever before. Families are navigating increasingly complex caregiving responsibilities. Housing needs evolve. Relationships shift. Financial priorities change.

The longer the retirement horizon, the more opportunities there are for life to challenge the original plan.

That's why preparation cannot simply be about creating documents.

It must also be about creating flexibility.

The Questions Every Family Should Consider

A truly prepared plan addresses more than assets.

It considers questions such as:

What happens if one spouse becomes a caregiver?

How will future care needs be funded and coordinated?

Is the current living arrangement sustainable long term?

Are family members aligned on expectations and responsibilities?

Can the plan absorb unexpected changes without creating unnecessary stress?

These are not estate planning questions.

They are life planning questions.

And they are often the questions that matter most.

Preparedness Is About Adaptability

Having documents doesn't mean a family is aligned.

Having a plan doesn't mean it will hold under pressure.

Preparation is not measured by how organized a binder looks on a shelf.

It is measured by whether the people involved know how to navigate change when it arrives.

The strongest plans are not the most rigid.

They are the most adaptable.

They acknowledge uncertainty.

They anticipate transitions.

They create space for life's inevitable surprises.

A Final Thought

The question isn't:

"Is the plan complete?"

The question is:

"Will this plan still work when life doesn't go as expected?"

Because true preparedness isn't found in paperwork alone.

It's found in the ability to move through life's transitions with clarity, flexibility, and confidence.

Continue the Conversation

Preparing for the future requires more than financial paperwork—it requires adaptability, resilience, and a deeper understanding of how longevity, technology, and life transitions are reshaping retirement itself.

These themes are explored further in Carroll S. Golden’s book, Leading in the New Retirement Era: How to Lead, Adapt, and Win in an AI-Driven World