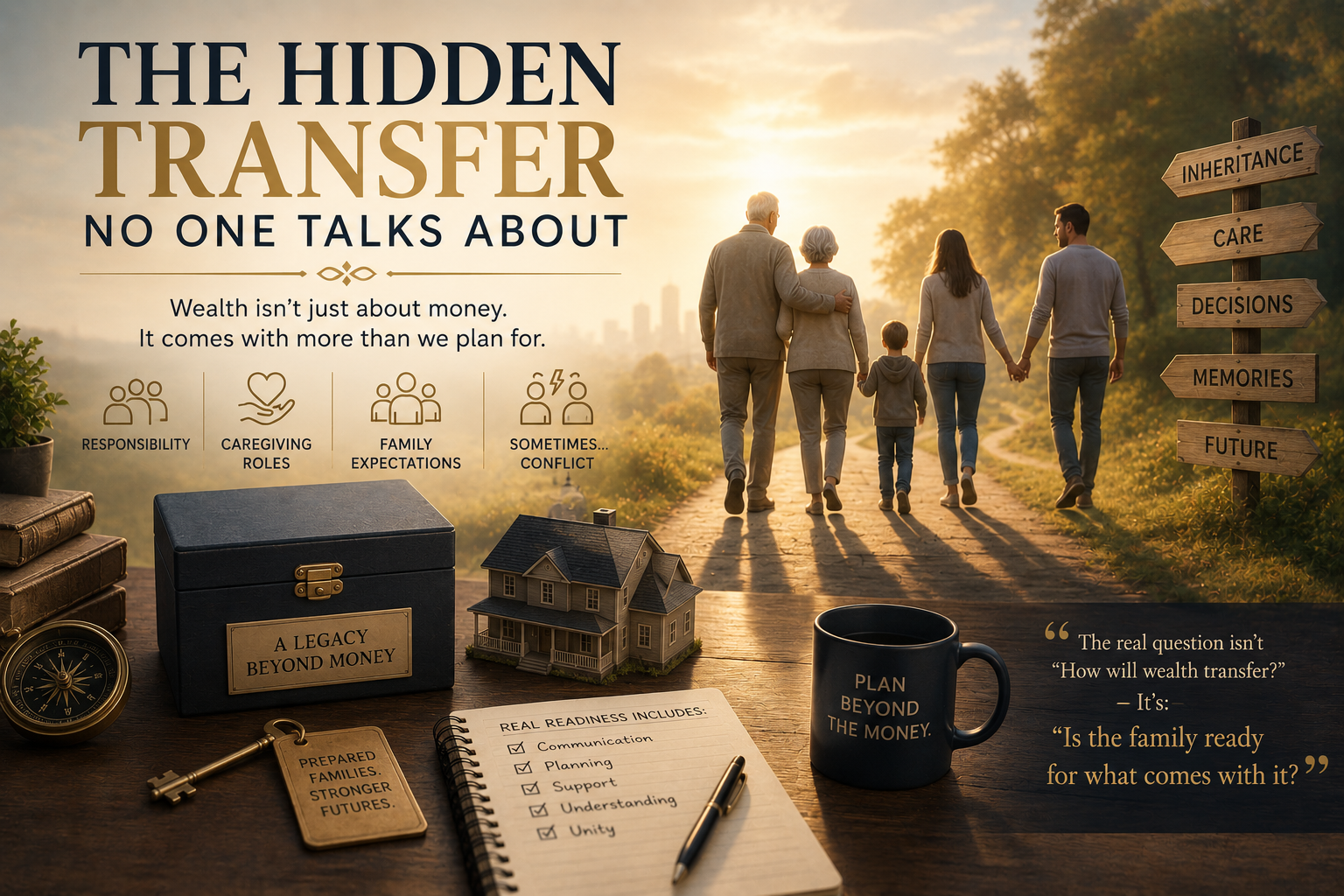

The Hidden Transfer No One Talks About

Retirement Strategist Carroll Golden

When people hear the phrase The Great Wealth Transfer, the conversation almost always centers on money.

And understandably so.

An estimated $124 trillion is expected to transfer between generations by 2048, making it one of the largest wealth transitions in modern history.

The headlines focus on the numbers.

The size of the assets.

The transfer of investment portfolios, retirement accounts, real estate holdings, and family wealth.

But there is an important reality that often gets overlooked:

The transfer of wealth is not simply a financial event.

It is a human event.

And money is rarely the most complicated part.

The Wealth Transfer We're Missing

When most people think about wealth transfer, they imagine assets moving from parents to children.

But in many cases, wealth moves sideways before it moves forward.

It transfers first to a surviving spouse—often a widow.

At that moment, the transfer involves far more than financial assets.

It can also bring:

Responsibility

Decision-making pressure

Caregiving obligations

Housing decisions

Family expectations

Emotional stress

Sometimes... conflict

The financial transfer and the life transition often happen simultaneously.

And that is where many plans begin to break down.

Money Rarely Arrives Alone

An inheritance may arrive during one of the most emotionally challenging periods of a person's life.

A spouse may suddenly find themselves responsible for managing finances they have never handled before.

An adult child may inherit assets while simultaneously coordinating care for an aging parent.

A family member may receive a home while also inheriting the responsibility of maintaining it, managing it, or deciding whether to sell it.

The asset arrives.

But so does the responsibility.

And that responsibility can sometimes feel far heavier than the money itself.

When Assets Become Complex

Certain assets carry emotional weight far beyond their financial value.

The family home is one of the clearest examples.

On paper, it may appear to be a valuable asset.

In reality, it can represent decades of memories, family history, caregiving responsibilities, and difficult decisions.

One person may view the home as an investment.

Another may view it as an obligation.

Another may see it as a symbol of family identity.

Suddenly, a financial asset becomes an emotional crossroads.

The same can be true for family businesses, vacation properties, heirlooms, and even investment accounts tied to family expectations.

Without communication and preparation, even well-intentioned inheritances can create confusion, stress, and family tension.

The Transfer of Responsibility

Perhaps the least discussed aspect of the Great Wealth Transfer is the transfer of responsibility.

As people live longer, caregiving responsibilities continue to expand.

Many families are navigating years—or even decades—of caregiving, healthcare coordination, housing transitions, and financial decision-making.

This creates a reality where the next generation often inherits more than money.

They inherit:

Caregiving roles

Medical decision responsibilities

Family leadership responsibilities

Emotional burdens

Time commitments

Financial obligations connected to care

If we only plan for the transfer of wealth, we miss the transfer of responsibility.

And that is where plans often fall short.

Why Longevity Changes Everything

Part of what makes the Great Wealth Transfer different from previous generations is that people are living longer.

Longer lives are one of society's greatest achievements. They create opportunities for extended careers, longer retirements, deeper family relationships, and additional years to pursue purpose and fulfillment.

But longevity also introduces complexity.

A longer life often means more healthcare needs, more caregiving responsibilities, and more financial decisions that must be managed over extended periods of time.

In previous generations, wealth transfer frequently occurred after relatively short retirements.

Today, families may spend years—or even decades—supporting aging parents while simultaneously helping adult children and grandchildren.

Many individuals find themselves in what is often called the "sandwich generation"—caring for older family members while still supporting younger ones.

As longevity increases, wealth transfer becomes less about a single event and more about an extended family transition.

The challenge is no longer simply passing assets from one generation to another.

The challenge is navigating the realities that accompany longer lives.

The Rise of the Family Caregiver

One of the most significant yet underappreciated aspects of modern wealth transfer is caregiving.

Millions of families are already providing support to aging loved ones through transportation, medical coordination, financial oversight, housing assistance, and daily care.

Yet many families never formally discuss who will assume these responsibilities when the need arises.

Caregiving often develops gradually.

A few doctor's appointments become regular appointments.

Occasional assistance becomes ongoing support.

A temporary situation becomes a long-term commitment.

By the time families recognize the magnitude of the responsibility, decisions are often being made under pressure.

This is why caregiving deserves a central place in planning conversations.

The financial impact can be significant.

The emotional impact can be even greater.

Families who proactively discuss caregiving expectations are often better positioned to navigate future challenges with greater clarity and less conflict.

Preparing People, Not Just Portfolios

Financial plans are designed to prepare assets for the future.

But who is preparing the people?

This may be one of the most important questions facing families today.

Many heirs inherit wealth without ever having meaningful conversations about family expectations, caregiving responsibilities, decision-making authority, or legacy intentions.

As a result, even carefully designed estate plans can leave family members feeling uncertain, overwhelmed, or unprepared.

Preparation should include more than legal documents and financial strategies.

It should also include:

Open family conversations

Shared understanding of future responsibilities

Discussions about caregiving preferences

Housing and lifestyle considerations

Clarity around decision-making roles

Understanding the emotional dimensions of inheritance

When families focus on both financial preparedness and human preparedness, they create a stronger foundation for navigating change.

Because ultimately, the goal is not simply to transfer wealth.

The goal is to help families thrive through the transition.

Why Modern Planning Must Go Beyond Assets

Traditional planning focuses heavily on accumulation, preservation, and distribution.

Those elements remain important.

But today's longevity landscape requires a broader perspective.

Families need plans that prepare not only for financial transitions but also for human transitions.

That means discussing:

Caregiving expectations

Family communication

Housing flexibility

Decision-making authority

Long-term care realities

Emotional preparedness

Because successful planning is not measured solely by how efficiently assets transfer.

It is measured by how well families navigate the realities that accompany that transfer.

The strongest plans recognize that wealth, relationships, caregiving, housing, and family dynamics are deeply connected.

Ignoring any one of these elements can create challenges that no legal document can fully solve.

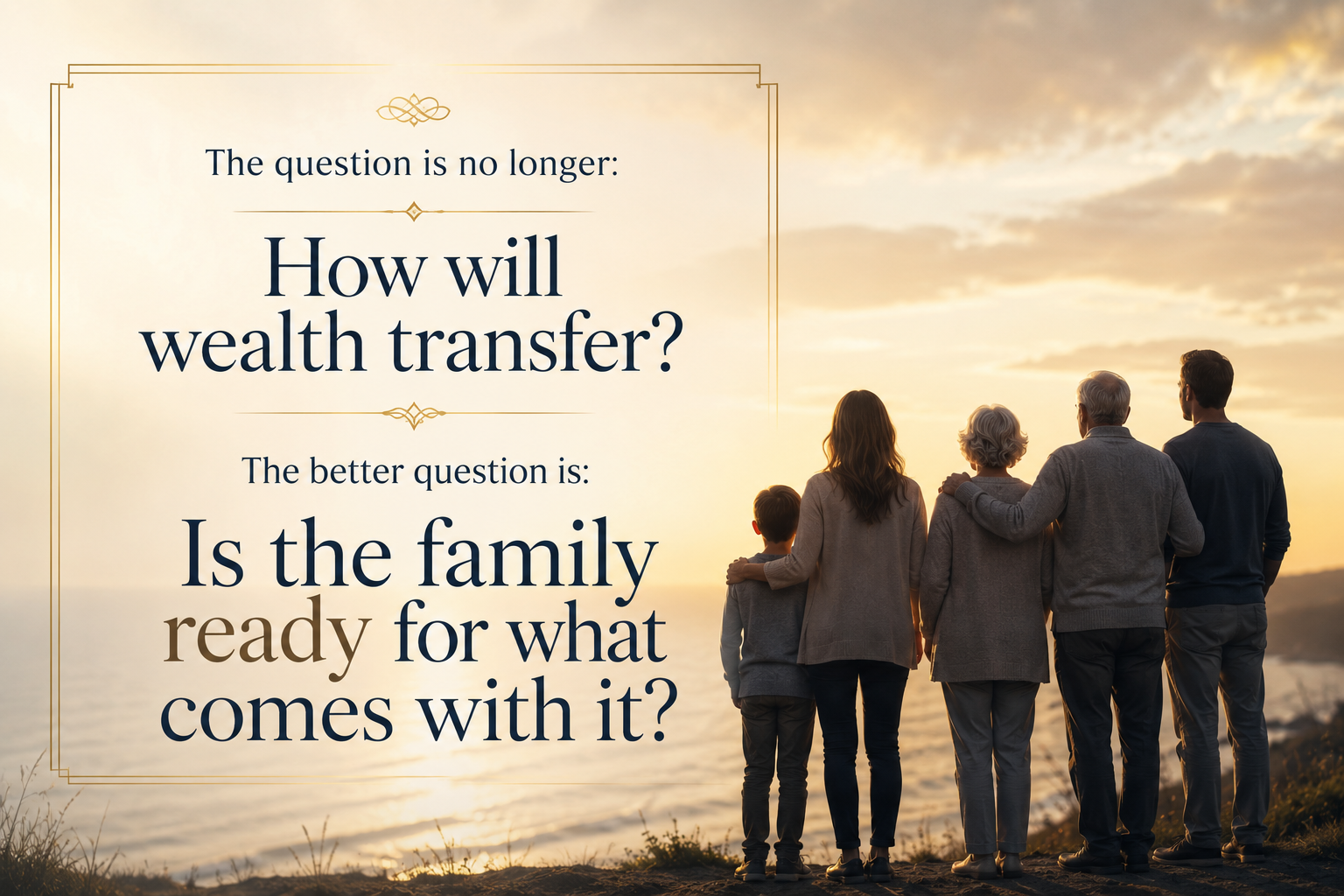

The Real Question

For years, the conversation has focused on one question:

"How will wealth transfer?"

But a more important question may be:

"Is the family ready for what comes with it?"

Because wealth does not move alone.

It arrives carrying responsibility, expectations, relationships, decisions, and emotions.

An inheritance can arrive at the exact moment someone becomes a caregiver.

A home can be both a financial asset and an emotional burden.

A surviving spouse can suddenly become responsible for major financial decisions while navigating grief and uncertainty.

These are the realities that often determine whether a transition succeeds or struggles.

And in the years ahead, the families that navigate the Great Wealth Transfer most successfully may not be those with the largest portfolios.

They may be the ones most prepared for the human realities that accompany the money.

Continue the Conversation

The future of planning is about more than wealth.

It is about longevity, caregiving, family dynamics, leadership, adaptability, and preparing for the realities of longer lives.

These themes are explored further in Leading in the New Retirement Era: How to Lead, Adapt, and Win in an AI-Driven World.

As retirement evolves and family responsibilities become more complex, the need for holistic planning has never been greater.

Because the most successful transitions are not defined solely by what is transferred.

They are defined by how well people are prepared for what comes next.